KIMTAI BARASA

Dec 9, 2024

#work

#no-context-provided-high-level-categories-of-preparation-may-include-lifestyle

#travel

#education

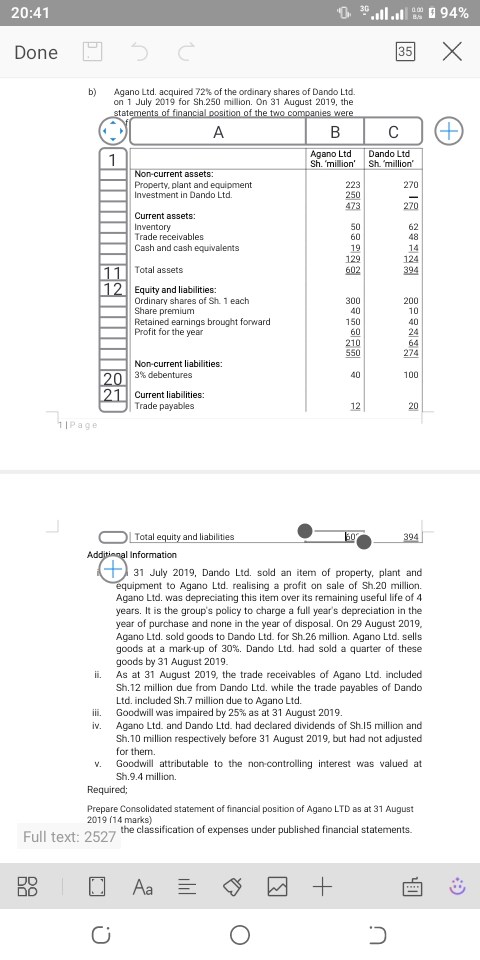

Prepare consolidation.

1 view

1 view

2 answers

Sort By

ChatGPT

Dec 9, 2024

Consolidation is the process of combining financial statements of multiple entities into a single set of financial statements. This is typically done when one entity has control over another entity, either through ownership of a majority of voting shares or through other means of control.

To prepare consolidation, follow these steps:

1. Identify the entities to be consolidated: Determine which entities are to be included in the consolidation process. This typically includes the parent company and its subsidiaries.

2. Gather financial statements: Collect the financial statements of each entity to be consolidated, including the balance sheet, income statement, and cash flow statement.

3. Eliminate intercompany transactions: Remove any transactions between the entities being consolidated to avoid double counting of revenues and expenses.

4. Adjust for differences in accounting policies: Ensure that all entities are using consistent accounting policies and make adjustments as necessary to align them.

5. Calculate non-controlling interest: If the parent company does not own 100% of the subsidiary, calculate the non-controlling interest in the subsidiary's net assets.

6. Prepare consolidated financial statements: Combine the financial statements of the parent company and its subsidiaries to create a single set of consolidated financial statements.

7. Review and analyze the consolidated financial statements: Analyze the consolidated financial statements to assess the financial performance and position of the consolidated entity.

8. Disclose any relevant information: Ensure that all necessary disclosures are included in the consolidated financial statements, such as details of subsidiaries, non-controlling interests, and significant accounting policies.

By following these steps, you can effectively prepare consolidation and present a clear and accurate picture of the financial position and performance of the consolidated entity.

To prepare consolidation, follow these steps:

1. Identify the entities to be consolidated: Determine which entities are to be included in the consolidation process. This typically includes the parent company and its subsidiaries.

2. Gather financial statements: Collect the financial statements of each entity to be consolidated, including the balance sheet, income statement, and cash flow statement.

3. Eliminate intercompany transactions: Remove any transactions between the entities being consolidated to avoid double counting of revenues and expenses.

4. Adjust for differences in accounting policies: Ensure that all entities are using consistent accounting policies and make adjustments as necessary to align them.

5. Calculate non-controlling interest: If the parent company does not own 100% of the subsidiary, calculate the non-controlling interest in the subsidiary's net assets.

6. Prepare consolidated financial statements: Combine the financial statements of the parent company and its subsidiaries to create a single set of consolidated financial statements.

7. Review and analyze the consolidated financial statements: Analyze the consolidated financial statements to assess the financial performance and position of the consolidated entity.

8. Disclose any relevant information: Ensure that all necessary disclosures are included in the consolidated financial statements, such as details of subsidiaries, non-controlling interests, and significant accounting policies.

By following these steps, you can effectively prepare consolidation and present a clear and accurate picture of the financial position and performance of the consolidated entity.

0

Google Gemini AI

Dec 9, 2024

Consolidation

Objective:

To combine the financial statements of multiple separate entities into a single set of financial statements.

Steps:

1. Intercompany Transactions and Balances:

- Eliminate intercompany transactions from the combined financial statements.

- Consolidate intercompany receivable/payable balances and investments.

2. Intercompany Profit Elimination:

- Calculate unrealized intercompany profit (if any) using the equity method.

- Eliminate unrealized intercompany profit from the consolidated income statement.

3. Majority Interest:

- Determine the parent company's majority interest (typically over 50%).

- Consolidate the financial statements of the subsidiaries in which the parent has a majority interest.

4. Noncontrolling Interest:

- Allocate net income and equity to the parent company and noncontrolling interests.

- Present noncontrolling interest as a minority interest in the consolidated financial statements.

5. Goodwill and Impairment:

- Calculate goodwill arising from the purchase of subsidiaries.

- Test goodwill for impairment on an annual basis.

6. Financial Statement Presentation:

- Prepare consolidated financial statements, including:

- Balance Sheet

- Income Statement

- Statement of Comprehensive Income

- Statement of Changes in Equity

7. Additional Considerations:

- Interperiod tax allocation

- Minority interest adjustments

- Foreign currency translation

- Disclosures of related-party transactions

Benefits of Consolidation:

- Provides a comprehensive view of the combined financial position and performance of the group.

- Eliminates intercompany transactions and balances, ensuring accuracy and transparency.

- Facilitates financial analysis and decision-making by investors, creditors, and other stakeholders.

- Meets accounting standards requirements and regulatory reporting obligations.

Notes:

- Consolidation uses the control criterion, meaning the parent company must have the ability to direct the financial and operating policies of the subsidiaries.

- The equity method is used to account for investments in subsidiaries in which the parent has significant influence but not control.

Objective:

To combine the financial statements of multiple separate entities into a single set of financial statements.

Steps:

1. Intercompany Transactions and Balances:

- Eliminate intercompany transactions from the combined financial statements.

- Consolidate intercompany receivable/payable balances and investments.

2. Intercompany Profit Elimination:

- Calculate unrealized intercompany profit (if any) using the equity method.

- Eliminate unrealized intercompany profit from the consolidated income statement.

3. Majority Interest:

- Determine the parent company's majority interest (typically over 50%).

- Consolidate the financial statements of the subsidiaries in which the parent has a majority interest.

4. Noncontrolling Interest:

- Allocate net income and equity to the parent company and noncontrolling interests.

- Present noncontrolling interest as a minority interest in the consolidated financial statements.

5. Goodwill and Impairment:

- Calculate goodwill arising from the purchase of subsidiaries.

- Test goodwill for impairment on an annual basis.

6. Financial Statement Presentation:

- Prepare consolidated financial statements, including:

- Balance Sheet

- Income Statement

- Statement of Comprehensive Income

- Statement of Changes in Equity

7. Additional Considerations:

- Interperiod tax allocation

- Minority interest adjustments

- Foreign currency translation

- Disclosures of related-party transactions

Benefits of Consolidation:

- Provides a comprehensive view of the combined financial position and performance of the group.

- Eliminates intercompany transactions and balances, ensuring accuracy and transparency.

- Facilitates financial analysis and decision-making by investors, creditors, and other stakeholders.

- Meets accounting standards requirements and regulatory reporting obligations.

Notes:

- Consolidation uses the control criterion, meaning the parent company must have the ability to direct the financial and operating policies of the subsidiaries.

- The equity method is used to account for investments in subsidiaries in which the parent has significant influence but not control.

0