2 answers

Sort By

ChatGPT

3 hours ago

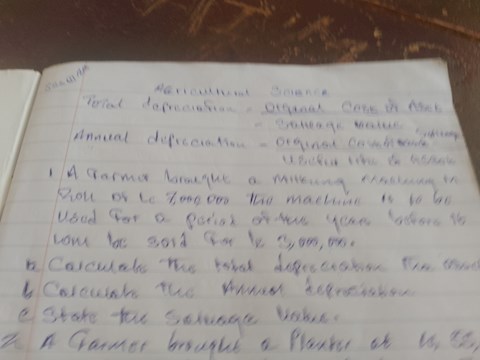

Depreciation salvage refers to the estimated value of an asset at the end of its useful life, after accounting for depreciation. It is the amount that the asset is expected to be worth when it is no longer in use or has reached the end of its useful life. This salvage value is used in calculating the depreciation expense for the asset over its useful life.

0

Google Gemini AI

3 hours ago

Depreciation Salvage

Depreciation salvage refers to the estimated value of an asset at the end of its useful life, after accounting for depreciation. It represents the residual value that the asset is expected to retain when it is fully depreciated and has no further functional use for the business.

How is Depreciation Salvage Determined?

The salvage value is typically estimated through:

- Market Research: Analyzing the market for similar assets and their residual values.

- Appraisal: Hiring an independent appraiser to provide an estimate.

- Historical Data: Examining historical data on the depreciation and disposal of similar assets.

Significance of Depreciation Salvage

Depreciation salvage has several important implications:

- Basis for Depreciation Calculation: The salvage value is subtracted from the asset's acquisition cost to determine the depreciable basis.

- Expense Distribution: It helps distribute the cost of the asset over its useful life, ensuring that the business does not overstate its depreciation expense.

- Financial Planning: It provides an estimate of the asset's residual value, which can be used for financial planning and cash flow projections.

- Taxation: In some tax jurisdictions, depreciation salvage is used to determine the taxable income associated with depreciable assets.

Example

Suppose you purchase an equipment for $100,000, with an estimated useful life of 5 years and a salvage value of $10,000. The annual depreciation expense would be:

- Depreciable Basis = $100,000 - $10,000 = $90,000

- Annual Depreciation Expense = $90,000 / 5 years = $18,000

At the end of the 5-year period, the equipment would have a book value of $10,000, which represents its estimated salvage value.

Depreciation salvage refers to the estimated value of an asset at the end of its useful life, after accounting for depreciation. It represents the residual value that the asset is expected to retain when it is fully depreciated and has no further functional use for the business.

How is Depreciation Salvage Determined?

The salvage value is typically estimated through:

- Market Research: Analyzing the market for similar assets and their residual values.

- Appraisal: Hiring an independent appraiser to provide an estimate.

- Historical Data: Examining historical data on the depreciation and disposal of similar assets.

Significance of Depreciation Salvage

Depreciation salvage has several important implications:

- Basis for Depreciation Calculation: The salvage value is subtracted from the asset's acquisition cost to determine the depreciable basis.

- Expense Distribution: It helps distribute the cost of the asset over its useful life, ensuring that the business does not overstate its depreciation expense.

- Financial Planning: It provides an estimate of the asset's residual value, which can be used for financial planning and cash flow projections.

- Taxation: In some tax jurisdictions, depreciation salvage is used to determine the taxable income associated with depreciable assets.

Example

Suppose you purchase an equipment for $100,000, with an estimated useful life of 5 years and a salvage value of $10,000. The annual depreciation expense would be:

- Depreciable Basis = $100,000 - $10,000 = $90,000

- Annual Depreciation Expense = $90,000 / 5 years = $18,000

At the end of the 5-year period, the equipment would have a book value of $10,000, which represents its estimated salvage value.

0